CreditRepair.com is a legitimate, registered credit repair company, but “legitimate” and “worth the monthly fees” are two very different things. The company has been in business since the mid-2000s and operates within the legal framework of the Credit Repair Organizations Act, which means it cannot charge you before performing services and must provide a written contract. However, the results it advertises — and the results customers actually experience — often diverge significantly. If you are expecting a service that will magically boost your score by 100 points in a few months, you are likely setting yourself up for disappointment and several hundred dollars in fees that could have been spent paying down the very debts dragging your score down.

The honest reality is that credit repair companies, CreditRepair.com included, can only do what you could legally do yourself for free: dispute inaccurate, unverifiable, or outdated information on your credit reports with the three major bureaus. A person with a legitimate error on their report — say, a medical collection that was already paid but never updated — might see meaningful improvement. Someone whose low score reflects accurate records of missed payments and high utilization is far less likely to see dramatic changes, no matter how many letters get sent on their behalf. This article breaks down what CreditRepair.com actually does, what realistic outcomes look like, where the marketing stretches the truth, and how to decide whether paying monthly fees makes sense for your specific financial situation.

Table of Contents

- Is CreditRepair.com Actually Legit or Just Another Credit Repair Scam Charging Monthly Fees?

- What CreditRepair.com Can Realistically Fix and Where It Hits a Wall

- Breaking Down the Actual Cost and What You Get for Monthly Fees

- DIY Credit Repair vs. Paying CreditRepair.com — A Practical Comparison

- The Marketing Claims That Should Make You Skeptical

- When Paying for Credit Repair Might Actually Make Sense

- What Actually Moves Your Credit Score More Than Disputes

- Conclusion

- Frequently Asked Questions

Is CreditRepair.com Actually Legit or Just Another Credit Repair Scam Charging Monthly Fees?

CreditRepair.com is not a scam in the legal sense. It is a real company with a physical address, a customer service operation, and a process that involves sending dispute letters to Equifax, Experian, and TransUnion on your behalf. It has historically been accredited or listed with the Better Business Bureau, though its rating and complaint volume have fluctuated over the years. The company also provides credit monitoring tools and a dashboard where you can track the status of disputes. On paper, that looks like a functioning service. Where things get murkier is in the gap between what the company implies you will achieve and what the fine print actually guarantees — which is nothing.

No credit repair company can legally guarantee specific score increases, and CreditRepair.com does include this disclaimer. But the marketing materials, testimonials, and sales calls tend to emphasize success stories that represent best-case scenarios rather than typical outcomes. A customer who had a single erroneous collection removed and saw a 40-point jump is real, but that experience is not representative of someone carrying three years of late payments across multiple accounts. It is also worth noting that the credit repair industry as a whole has drawn scrutiny from the Consumer Financial Protection Bureau and the Federal Trade Commission. Several credit repair companies have faced enforcement actions over the years for deceptive practices. As of recent reports, CreditRepair.com has not been the subject of a major federal enforcement action, but the broader industry context matters. When you are evaluating any credit repair service, the baseline question should not be “is this company legal” but rather “can this company do something I cannot do myself, and is that worth the ongoing cost?”.

What CreditRepair.com Can Realistically Fix and Where It Hits a Wall

The core service CreditRepair.com provides is filing disputes with the credit bureaus under the Fair Credit Reporting Act. This law gives every consumer the right to challenge information on their credit report that they believe is inaccurate, incomplete, or unverifiable. The bureau then has 30 days to investigate, and if the furnisher — the creditor or collector who reported the item — cannot verify it, the item must be removed. CreditRepair.com systematizes this process, sending multiple rounds of dispute letters and following up on responses. This works well when there are genuine errors on your report. Mistaken identities, debts that were paid but still show as outstanding, duplicate entries, accounts opened through identity theft, and outdated collections that should have aged off are all fair game. If your credit report has these kinds of issues, a dispute process — whether you do it yourself or pay someone — can produce real results.

However, if the negative items on your report are accurate and verifiable, the dispute process has severe limitations. A creditor who correctly reported that you were 90 days late in 2024 can simply verify that information, and the item stays. Some credit repair companies send disputes anyway hoping that a furnisher will fail to respond within the 30-day window, but the bureaus and creditors have gotten significantly better at responding to disputes over the years, and this strategy produces diminishing returns. The important caveat here is timing. Even items that are removed through a successful dispute can sometimes reappear if the furnisher later verifies the information. This is legal under the FCRA as long as the bureau notifies you. So a customer might see a score bump after a round of disputes, only to watch some of those gains erode a month or two later. CreditRepair.com does not typically highlight this possibility in its marketing.

Breaking Down the Actual Cost and What You Get for Monthly Fees

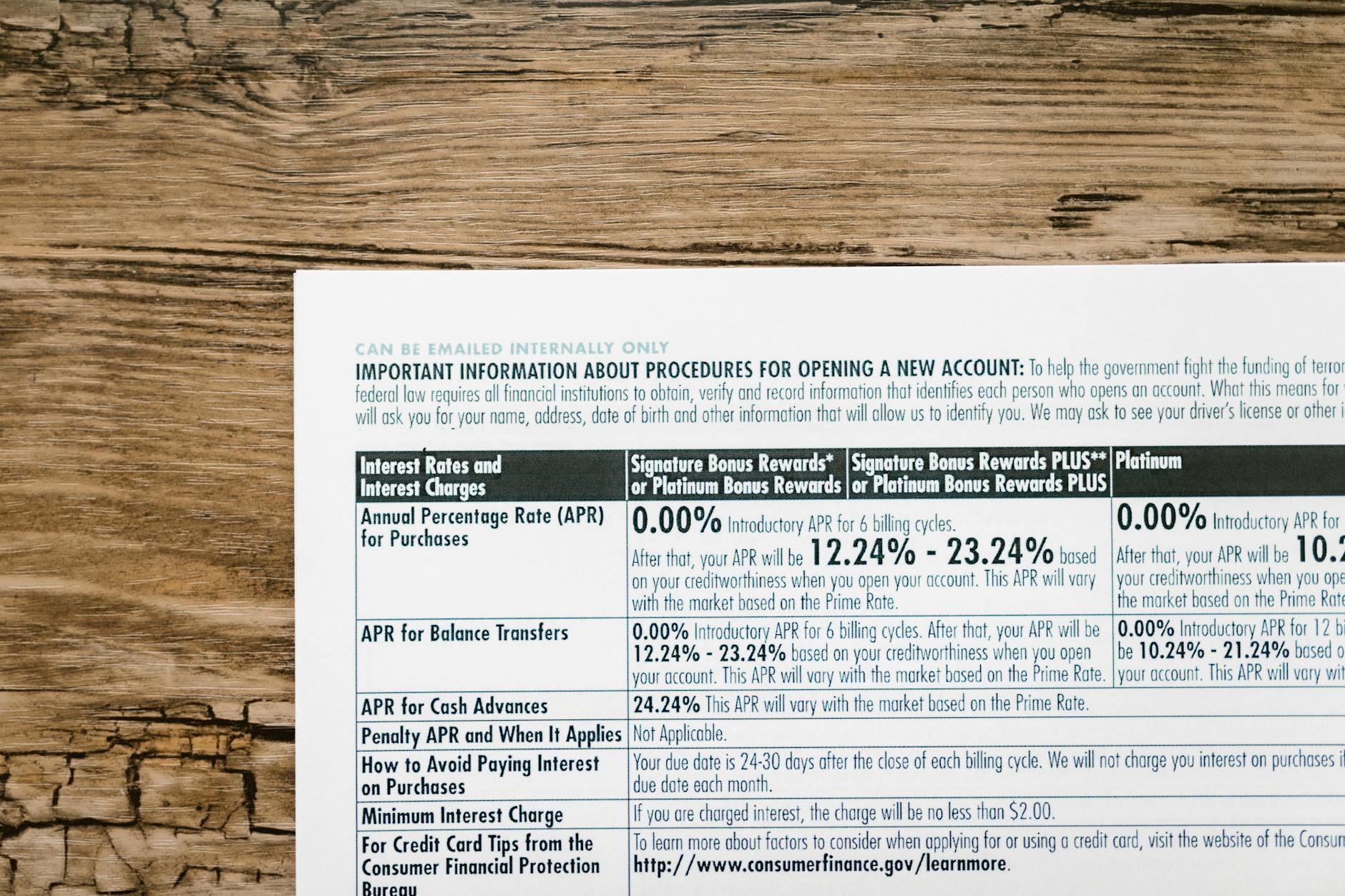

CreditRepair.com has historically offered tiered pricing plans, though the exact prices and plan names have changed over the years. As of recent reports, the company has typically charged somewhere in the range of $50 to $100 or more per month depending on the service level, often with a first-work fee or setup charge on top of the monthly subscription. The higher-tier plans generally include more disputes sent per cycle, additional creditor interventions such as goodwill letters, and extras like identity theft insurance or more frequent score updates. Here is where the math gets uncomfortable for a frugal-minded person. If you stay enrolled for six months at a mid-tier plan, you might spend somewhere in the range of $500 to $700 or more, depending on current pricing. For that money, you are primarily paying for someone to write and mail dispute letters — something you can do yourself using free templates from the CFPB’s website and the credit bureaus’ own online dispute portals.

The additional tools like credit monitoring are available for free through services like Credit Karma, your bank’s app, or AnnualCreditReport.com. The question is not whether CreditRepair.com provides a real service but whether the convenience of having someone else handle the paperwork is worth what could amount to a month or two of aggressive debt paydown instead. One thing to watch carefully is the cancellation process. Credit repair subscriptions are notoriously sticky. Some customers have reported difficulty canceling or being talked into staying enrolled for “just one more cycle.” Before signing up, make sure you understand exactly how to cancel and that you will not be charged after cancellation. Document everything in writing.

DIY Credit Repair vs. Paying CreditRepair.com — A Practical Comparison

If you are weighing whether to handle credit repair yourself or pay for it, consider what each path actually involves. The DIY route requires you to pull your credit reports from all three bureaus through AnnualCreditReport.com, go through each line item looking for errors, draft dispute letters or use the online dispute portals, mail them via certified mail if you want a paper trail, track responses, and follow up as needed. This process is not complicated, but it is tedious and requires you to stay organized over several months. For someone who is comfortable with paperwork and has the time, this is the clear financial winner since the only cost is postage. CreditRepair.com’s advantage is convenience and systematization. The company has templates, tracking software, and staff who do this routinely.

If you are overwhelmed by your financial situation, working multiple jobs, or simply do not trust yourself to follow through on a months-long administrative process, paying someone to manage it has real value — similar to paying a tax preparer when you could technically file yourself. The tradeoff is straightforward: you are paying a premium for execution, not expertise. There is no secret technique or insider access that credit repair companies have. They use the same laws and the same dispute process available to every consumer. A middle-ground option that many personal finance advisors suggest is using a nonprofit credit counseling agency. Organizations affiliated with the National Foundation for Credit Counseling offer free or low-cost credit report reviews and can help you understand what is fixable and what is not. They will not file disputes for you in most cases, but they can help you build a plan and avoid paying for a service that may not move the needle in your situation.

The Marketing Claims That Should Make You Skeptical

Credit repair marketing — across the entire industry, not just CreditRepair.com — relies heavily on before-and-after score testimonials. You will see claims like “removed 15 negative items” or customer stories showing 100-plus point score increases. These are typically real customers, but they represent outlier results, not averages. The customers most likely to see dramatic improvements are those who had significant errors on their reports — identity theft victims, people with incorrectly reported medical debts, or those with outdated items that should have fallen off. If your situation involves accurate negative information, temper your expectations considerably. Be particularly wary of any language suggesting the company can remove accurate negative information. Under the FCRA, accurate and verifiable information can legally remain on your credit report for seven years (10 years for bankruptcies).

No credit repair company can override this. If a salesperson implies otherwise — even indirectly through phrases like “we challenge everything” or “the bureaus often can’t verify older items” — that is a red flag. The FTC has specifically warned consumers that companies promising to remove accurate negative information are likely engaging in deceptive practices. Another common marketing tactic is urgency. Phrases like “every month you wait costs you money” or “your score could be higher by next month” create pressure to sign up immediately. While it is true that a higher credit score can save you money on interest over time, the decision to pay for credit repair should be made deliberately, not impulsively. Pull your free credit reports first, identify what is actually wrong, and then decide whether you need help fixing it.

When Paying for Credit Repair Might Actually Make Sense

There is a narrow set of circumstances where paying for a credit repair service can be defensible. If you are a victim of identity theft with dozens of fraudulent accounts across all three bureaus, the sheer volume of disputes can be overwhelming, and having a service manage the process might save you significant stress. Similarly, if you are preparing for a major financial event — buying a home within the next year, for example — and you have identified specific errors that are suppressing your score, the time savings of professional help could translate into real money saved on a mortgage rate.

In that scenario, the monthly fees might pay for themselves many times over in lower interest charges. But even in these cases, you should set a hard deadline for how long you will stay enrolled. Three to six months is a reasonable window to see whether disputes are producing results. If your score has not meaningfully changed after that period, continuing to pay is unlikely to yield different outcomes, and you are better off redirecting that money toward paying down balances or building positive credit history with a secured card.

What Actually Moves Your Credit Score More Than Disputes

The uncomfortable truth that no credit repair company wants to emphasize is that for most people with low credit scores, the fastest path to improvement is not disputing items — it is changing the financial behaviors that produced the low score in the first place. Payment history and credit utilization together account for roughly two-thirds of most credit scoring models. Making every payment on time going forward and reducing your credit card balances below 30 percent of your limits — ideally below 10 percent — will almost always produce more score improvement than a dispute-letter campaign targeting accurate negative marks.

Looking ahead, the credit reporting landscape continues to shift. Recent years have seen medical debt under a certain dollar threshold removed from credit reports, and there is ongoing regulatory pressure to further limit the impact of medical collections and certain other categories. These changes have helped millions of consumers without any credit repair intervention at all. Staying informed about these shifts through the CFPB’s website is free and may be more valuable than any monthly subscription.

Conclusion

CreditRepair.com is a real company offering a real service, but the value proposition is thin for most consumers. The disputes it files are the same ones you can file yourself for free, the credit monitoring it bundles is widely available at no cost, and the results it can achieve are fundamentally limited by what the law allows — which is the removal of inaccurate or unverifiable information only. If your credit problems stem from accurate negative history, no amount of monthly fees will change that. The money spent on a six-month subscription could instead go toward paying down a credit card balance, which would likely do more for your score than any dispute letter.

Before paying anyone for credit repair, pull your reports for free, identify exactly what is dragging your score down, and determine whether those items are errors or accurate reflections of your history. If they are errors, you can dispute them yourself or, if the volume is truly overwhelming, consider a short and strictly time-limited engagement with a credit repair service. If they are accurate, save your money. Put it toward debt reduction, set up autopay so you never miss a due date again, and give your score time to recover naturally. That is the unsexy, unglamorous, unmarketed truth about credit repair — and it is the advice that will actually save you money.

Frequently Asked Questions

Can CreditRepair.com remove late payments from my credit report?

Only if the late payments were reported in error. If your creditor correctly reported that you paid late, the company can dispute it, but the creditor will likely verify the information and it will remain on your report for up to seven years from the date of the late payment.

How long does it take to see results from CreditRepair.com?

The credit bureaus have 30 days to investigate each dispute, so the earliest you might see any changes is about 30 to 45 days after disputes are filed. Meaningful results, if they are going to happen, typically show up within three to six months. If nothing has changed after six months, continuing to pay is unlikely to produce different outcomes.

Can I cancel CreditRepair.com at any time?

Credit repair companies are required by federal law to allow cancellation without penalty. However, some customers have reported that the cancellation process involved retention calls or delays. Document your cancellation request in writing and confirm in writing that your account has been closed and no further charges will be applied.

Is it illegal to dispute accurate information on my credit report?

It is not illegal for you to dispute anything on your credit report — the FCRA gives you broad dispute rights. However, knowingly filing false disputes or using deceptive tactics to get accurate information removed can create legal issues, and any credit repair company that encourages this is operating unethically.

Will credit repair hurt my credit score?

The dispute process itself does not lower your score. However, if disputes are resolved in a way that updates account information — for example, confirming a balance you were hoping to get removed — that updated information could affect your score. In most cases, the process is either neutral or positive.